In a circular dated December 29, 2025, the Federal Ministry of Finance announced changes to fields in, among other things, the

- 2026 advance VAT return

- 2026 yearly VAT return

- special advance payment of VAT for 2026

- income tax return 2025.

Specifically, this concerns editorial changes in “field 500”. In our view, these changes pose new challenges for those who submit and are responsible for tax returns and declarations, as well as for taxpayers, as there is a conflict between transparent reporting or declaration and criminal tax law.

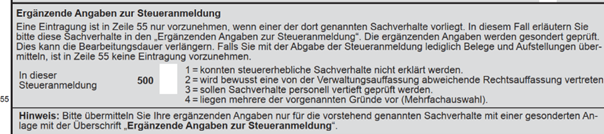

What exactly does the editorial change in field 500 mean?

The previously known codes (e.g., code 23 in the VAT return), which were used to refer to additional supporting documents and an accompanying letter, are now being replaced by the tax authorities e.g. by the new code 500 in the advance VAT return form, which divides "supplementary information" on the tax return into four categories:

- Category: Tax-relevant facts could not be declared.

- Category: Deliberate deviation from the administrative opinion due to a different legal opinion.

- Category: Facts are to be examined in depth by personnel of the tax authorities.

- Category: Multiple selections from categories 1 to 3.

Example from the 2026 VAT return form (in German, highlights mainly the above described categories):

Just reading these four categories raises the question of which cases are covered by the categories of the new code 500 and what advantages or risks arise from using the code.

When code 500 is used, the tax return or tax declaration submitted is excluded from automated processing (implementation of the mandate in Sect. 150(7) of the General Tax Code, Sect. 155(4) of the General Tax Code). This can lead to longer processing times. This is expressly pointed out in the form field. In the area of VAT in particular, this can also mean that, depending on the processing time required by the responsible tax officer, a refund will only be issued after the manual review has been completed. Under certain circumstances, this can lead to financial disadvantages, as a company cannot use of the refund amount in the event of an input tax surplus during this waiting period for the separate review. It remains to be seen how the processing time will develop in practice. Depending on how intensively the code is used in practice, the question then arises as to how the processing time will develop if, in the worst case scenario, the financial administration does not have sufficient human resources to carry out a swift check.

In addition, the question arises as to whether these categories must be ticked on every cover letter. Are cover letters without the corresponding tick still acceptable from the point of view of the tax authorities? What are the criminal tax implications associated with their respective use? Because one thing remains constant: The legal obligation to submit tax returns or tax declarations correctly and completely (Sect. 90(1) sent. 2 of the General Tax Code).

Please note: Code number 500 also has criminal law relevance

Code number 500 is therefore not a normal form field. Rather, it (also) has criminal relevance that should not be underestimated. Regardless of whether the box is checked or not, there are criminal risks.

For example, failure to check the box, even though relevant information is available under code number 500, can be interpreted as deliberate concealment. This can quickly lead to suspicion of intentional action. Particularly in cases of unclear circumstances, diverging legal opinions, or atypical input tax constellations, failure to check the box can be interpreted as concealment of essential information or as an attempt to circumvent automated risk control and thus a manual audit.

Even a supplementary attachment to the tax return does not completely dispel this impression, as without a cross being placed, the procedural control function – which is clearly intended by the tax authorities and required by Sect. 150(7) of the General Fiscal Code – is lost. This circumstance can then be used as an indication that a manual check was deliberately prevented, even though the facts set out in the attachment and the corresponding classification under code 500 were known.

However, placing a cross should also be carefully considered. It is true that the accusation of intent can be rejected by referring to the transparent information provided. However, a cross automatically triggers an in-depth manual check ("cause" within the meaning of Sect. 155(4) sent. 3 of the General Fiscal Code), which, despite the previous entry under code number 500, can lead to criminal tax proceedings. In addition, there is a risk of being accused of submitting a tax return or tax declaration despite existing uncertainties or unclarified valuation aspects (as indicated by the cross). This can be interpreted by the tax authorities as a lack of diligence and as a sign of reckless tax evasion.

The meaning of fields 500 = 1 to 4

Code number 500 = 1 covers cases in which tax-relevant facts are established in the advance return period or assessment period but cannot yet be fully explained objectively. This does not refer to mere delays in the document flow, but to situations in which the applicable tax base cannot actually be finally determined at the time of filing. These cases typically occur (significantly) more frequently in cases of tax returns that must be submitted at short notice, such as those under Sect. 18(1) sent. 1 of the VAT Act, than in the case of income tax returns, for which there is a longer submission deadline (Sect. 149(2) of the General Fiscal Code). In addition, there are higher requirements for taxpayer cooperation, particularly in cases where it is particularly difficult to determine the "tax-relevant facts." This applies in particular to cases with international implications (Sect. 90(2) of the General Fiscal Code; Sect. 17 of the Foreign Transactions Tax Act (“AStG”); Sect. 12 of the Tax Heaven Defence Act (“StAbwG”)).

Typical examples in the area of VAT are, for example, reverse charge situations where the service has been provided but the final assessment basis has not yet been determined, bulk credits or returns at the end of the period where the allocation to tax rates has not yet been completed, or system and ERP conversions where certain sales tax allocations cannot yet be fully mapped for technical reasons.

This category is particularly sensitive in terms of criminal tax law. Anyone who submits an advance return or tax return in the knowledge that it is objectively incomplete without pointing this out suggests completeness. As noted above, this can be considered intentional action. The use of code number 500 = 1 can have an exonerating effect here, but it is essential that an appendix clearly states which points are still open and that a prompt correction will be made in accordance with Sect.153 of the General Fiscal Code.

Code number 500 = 2, on the other hand, does not refer to incompleteness, but to a conscious decision in favor of a different legal opinion. All relevant facts are available, but the taxpayer classifies them differently from the administrative opinion or, at least, from what could correspond to it. Examples of this are the declaration of an intra-Community supply as tax-exempt despite the lack of a VAT identification number, the distinction between supply and other services in the case of complex project or IT services, or the choice of a specific input tax allocation scale in accordance with Sect. 15(4) of the VAT Act.

Compared to an entry of "1" for code number 500, number "2" is significantly more relevant for income tax purposes. Divergent legal opinions that exist in cases with a clear "fact pattern" arise here, to give one example, in the question of whether the crediting of previous ownership periods under Sect. 4(2) of the Reorg Tax Act (“UmwStG”) in the case of reorgs also affects the points in time required by Sect. 9 No. 2a, 7 of the Trade Tax Act (“GewStG”).

This category in particular has a central protective function under criminal law. If such a legal position is taken without disclosure, there is regularly a considerable risk of being accused of tax evasion. If, on the other hand, the disclosure is complete and comprehensible, there is generally no intent. The code number 500 = 2 should therefore always be used when there is a conscious deviation from circulars by the Federal Ministry of Finance, application decrees such as the VAT application decree (“UStAE”), or established administrative practice. The accompanying annex should describe the facts in full, clearly state your own legal assessment, and disclose the quantitative effects.

Finally, in our opinion, code number 500 = 3 is intended for cases in which the advance return or tax return is complete and legally correct, but would appear unusual or conspicuous without explanation. As a rule, this is a matter of plausibility, not of dispute or ambiguity. Here, the facts are clear and complete, the assessment may be difficult, but it does not deviate from administrative opinion. Typical scenarios include, for example, high input tax surpluses due to one-off investments, exceptional jumps in sales due to final invoices or one-off orders, or collective corrections that distort the figures for a single month. In terms of criminal tax law, this category is relatively uncritical as long as it is not used to "cover up" facts that are actually incomplete or legally disputed. In addition, cases could fall under this category in which invoices do not necessarily entitle the taxpayer to an input tax deduction beyond doubt, but it can be argued that the service description is sufficient and that an audit by the tax authorities is appropriate, or, for example, it is assumed that a business has been sold in its entirety, but the case is not entirely clear, there is no deviation from the administrative opinion, and therefore a timely audit by the tax authorities should be carried out.

Note: It is interesting to note that a special personnel review should be carried out, but in cases where the legal assessment is not clear, according to the General Fiscal Code, only a binding commitment within the meaning of Sect. 204 of the General Fiscal Code or binding ruling within the meaning of Sect. 89 of the General Fiscal Code (provided that the facts of the case are established) can establish a legal claim and subsequent protection of legitimate expectations. This means that, from a purely legal point of view, the review does not lead to protection of legitimate expectations and may be reassessed later by the tax authorities in the context of a tax audit.

Code number 500 = 4, finally, is intended for cases in which at least two of the cases listed in Nos. 1 to 3 apply together. The combination of No. 2 and No. 3 should be relatively uncritical if there is a differing legal opinion and a special personal audit is to be carried out. Critical, on the other hand, are cases in which there is a combination of No. 1 and No. 3, i.e., an incomplete declaration of tax-relevant facts, in which a special personal audit is desired. In case of doubt, this case signals that a taxpayer is not in a position to report tax-relevant facts and is also requesting a special audit.

The General Fiscal Code only provides for the possibility of informing the tax office that a declaration is incorrect or incomplete in individual cases. These cases are regulated in Sect. 153 of the General Fiscal Code and open up the possibility of informing the tax office that tax-relevant facts have been identified but still need to be finally determined. This special case should generally only be reported by knowledgeable persons within the company or in consultation with and accompanied by a tax advisor or lawyer to ensure that the requirements for an effective correction of returns under Sect. 153 of the General Fiscal Code are not forfeited.

It remains to be seen how the tax authorities will deal with the use of code number 500 and, in particular, how the tension between criminal tax law and transparent declaration will play out in practice. Developments should be closely monitored. Whether and how the administrative and criminal investigation department or the public prosecutor's office will become more involved in cases of doubt is currently not foreseeable.

Recommendation for practice

In our view, the use of code number 500 with its four case variants means in practice that

- Code number 500 = 1 should only be used in exceptional cases and with tax law/criminal tax law advice,

- Code number 500 = 2 requires a detailed accompanying letter, as before,

- Code number 500 = 3 should be checked if a special audit is desired

- Code number 500 = 4, provided that code number 500 = 1 also applies, should also only be used in exceptional cases and with advice on tax law/criminal tax law.

In all cases, a cover letter with the subject line "Supplementary information on the tax return" or "Supplementary information on the tax declaration" is mandatory.

-

Katharina Lehner Katharina Lehner works as a lawyer and tax adviser on VAT at our Munich office. She has more than 15 years of experience in advising clients of all sizes on national and international VAT issues.

Katharina Lehner Katharina Lehner works as a lawyer and tax adviser on VAT at our Munich office. She has more than 15 years of experience in advising clients of all sizes on national and international VAT issues.View Profile -

Dr Martin Weiss Dr Martin Weiss is a tax adviser and a Certified Adviser in International Taxation, with many years of experience in advising companies on national and international tax law, inbound and outbound investments, tax structuring, and restructuring.

Dr Martin Weiss Dr Martin Weiss is a tax adviser and a Certified Adviser in International Taxation, with many years of experience in advising companies on national and international tax law, inbound and outbound investments, tax structuring, and restructuring.View Profile -

Wiebke Werner Wiebke Werner is Counsel at Grant Thornton Rechtsanwaltsgesellschaft mbH in Düsseldorf, working in the area of IT/IP, data privacy and digital innovation. She is a specialist lawyer for criminal law and a certified data protection officer.

Wiebke Werner Wiebke Werner is Counsel at Grant Thornton Rechtsanwaltsgesellschaft mbH in Düsseldorf, working in the area of IT/IP, data privacy and digital innovation. She is a specialist lawyer for criminal law and a certified data protection officer.View Profile