German Federal Fiscal Court confirms potential 0% withholding tax relief for US S-Corporations and comparable hybrid structures.

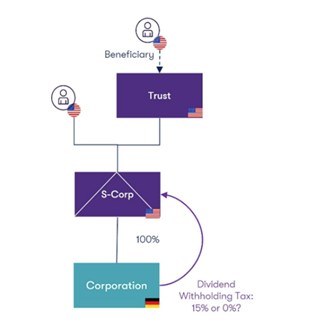

In a decision published recently (BFH dated 11 March 2026 – I R 13/23), the German Federal Fiscal Court (Bundesfinanzhof – BFH) confirmed that the participation exemption under Art. 10(3) of the US–Germany Double Tax Treaty (“DTT US”) may also apply to qualifying US S-Corporation (“S-Corp”) structures. The decision may also have implications for certain US LLC structures and other hybrid entities.

Uncertainty regarding eligibility for 0% treaty relief vs. 15% withholding tax for US S-Corporations

Dividend distributions by German corporations are generally subject to German withholding tax (“WHT”) of 26.375% (including solidarity surcharge). Under the DTT US, the WHT rate may generally be reduced:

- to 15% for individual US shareholders,

- to 5% for certain corporate shareholders, and

- potentially to 0% under Art. 10(3) DTT US.

The 0% rate may apply where:

- the US corporation directly holds at least 80% of the voting rights in the German corporation for at least 12 months; and

- the additional requirements of the Limitation-on-Benefits provision under Art. 28 DTT US are satisfied.

Reduced WHT rates generally require a formal application for relief—either via an exemption application (Freistellungsantrag) for future distributions or a refund application (Erstattungsantrag) for WHT already withheld.

The case addresses a long-standing controversy regarding hybrid entities such as US S-Corporations. While S-Corporations are treated as corporations from a German tax perspective, they are typically regarded as fiscally transparent entities for US tax purposes. This discrepancy raised the question whether treaty relief must be assessed solely at shareholder level—potentially resulting in a 15% WHT rate where the shareholders are US individuals—or whether the structure may nevertheless qualify for the 0% participation exemption under Art. 10(3) DTT US.

German tax authorities (BZSt) had generally denied the application of the 0% exemption in such cases and limited relief to 15%.

BFH confirms 0% treaty relief for qualifying S-Corporations and clarifies shareholder-level procedure

The BFH has now rejected this administrative view and confirmed that Art. 10(3) DTT US may apply to qualifying S-Corporation structures in light of Art. 1(7) DTT US.

Accordingly, the 0% rate may potentially be available even where all shareholders of the S-Corporation are US individuals, provided that the income derived by the company is taxed in the United States at the level of its US-resident shareholders as income of US residents.

Furthermore, the BFH clarified that treaty relief must not be claimed by the S-Corp itself, but rather by the US shareholders to whom the dividend is attributed for US tax purposes pursuant to Sec. 50d para. 1 sentence 11 German Income Tax Act (EStG) (old version). This reasoning should generally also apply under the current Sec. 50d para. 11a EStG.

Practical implications

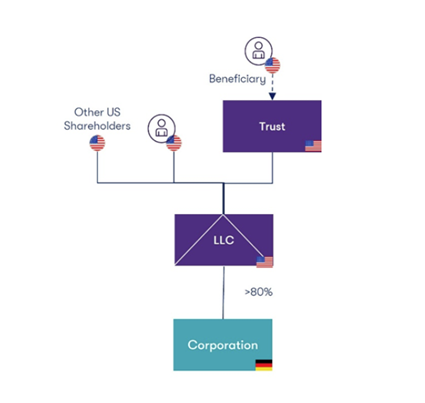

The decision is highly welcome for US investors using S-Corporation structures. Furthermore, it may also affect similar structures where the direct shareholder and recipient of the dividend is treated as a corporation for German tax purposes, but as a fiscally transparent or disregarded entity for US tax purposes.

Typical cases may involve certain US LLC structures, as the tax treatment of a US LLC must be determined on a case-by-case basis under the German legal form comparison test (Rechtstypenvergleich).

At the same time, it remains to be seen whether and how the German Ministry of Finance (Bundesministerium der Finanzen – BMF) and the BZSt will respond through administrative guidance or legislative changes.

In practice, the following aspects should additionally be considered:

- Who must file the WHT relief application?

Based on the BFH decision, the application should generally be filed by the US person or entity to whom the dividend is attributed for US tax purposes. - Timing of 0% relief – exemption vs. refund procedure

According to the current view of the BZSt, this may depend on the specific variant of Art. 10(3) DTT US. In certain cases, only a partial exemption (e.g. to 5% or 15%) may initially be granted within the exemption procedure, whereas the subsequent reduction to 0% may only be claimed following the actual distribution and withholding of WHT through a separate refund application. Due to the often significant processing times of refund applications, this may have a substantial cash flow impact. - Disregarded German distributing entities

It should further be noted that where the German distributing entity itself is treated as a disregarded entity for US tax purposes following a check-the-box election, it currently remains unclear whether treaty relief will be granted at all. In such cases, there is a risk that the full German dividend WHT of 26.375% may ultimately apply without any treaty relief. According to current administrative practice, the BZSt is still coordinating these cases with the IRS.

The further development of this topic remains highly relevant for German–US investment structures and withholding tax planning.

We would be happy to advise on the implications of this decision, including potential investment structures involving US LLCs or other hybrid entities as shareholders of German corporations. Feel free to reach out if this topic may be relevant for your structure.

Authors

-

Tobias Behrens

Tobias Behrens is a Tax Adviser and Manager in the International Tax subservice line at Grant Thornton.View Profile -

Lukas Kawka

Lukas Kawka is a Partner, lawyer and tax adviser in the Tax service line at our Berlin office. He has many years of expertise in providing tax advice to national and multinational companies.View Profile